AU & NZ

AU & NZ

SG

SG

MY

MY

US

US

IE

IE

Gift Aid rules for charities: the definitive overview

Your charity is doing important work, and Gift Aid is one of the most powerful ways to make every donation go further.

In fact, UK charities received £1.7 billion in Gift Aid in the year to April 2025, up 7% on the year before.

But, as much as £560 million still goes unclaimed every year – and the most common reason isn't bad intentions, it's simply not being sure of the rules.

Whether you're new to Gift Aid or want to make sure you're across the 2026 updates, here you'll find everything you need to tackle the Gift Aid rules for charities.

First, what is Gift Aid?

"Gift Aid is extremely valuable… but it is underused by donors and can be complicated for charities to claim. When an eligible taxpayer donates and forgets to tick the box, the charity misses out."

- Mark Greer, Managing Director, Charities Aid Foundation

Gift Aid was introduced in 1990 to make charitable giving more tax-efficient, and it remains one of the best income-boosting tools available to your charity.

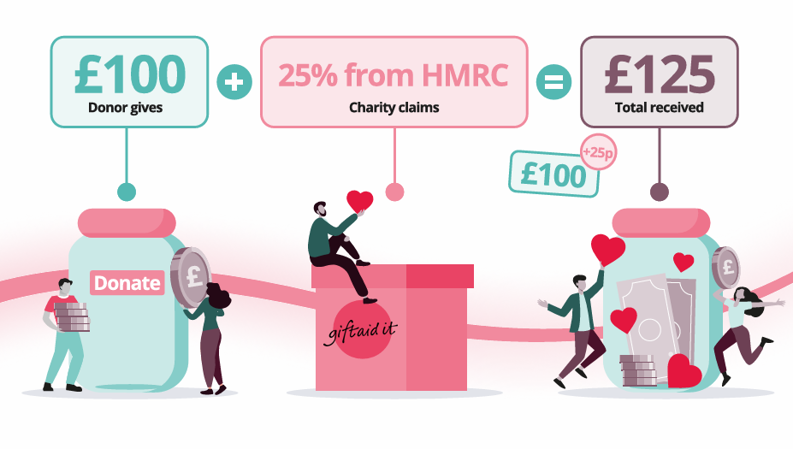

When an eligible UK taxpayer donates to you, they've already paid tax on that money. Gift Aid lets you reclaim that tax from HMRC, turning a £100 donation into £125, without your donor spending an extra penny.

The good news is that once you understand the rules, claiming confidently becomes much more straightforward, so let's walk through them.

What are the three eligibility questions?

Before you can claim Gift Aid on a donation, three things need to be true. Think of them as your checklist, and all three need a tick.

-

Is your organisation eligible?

Your charity must be a registered UK charity or community amateur sports club (CASC) and recognised by HMRC. Note: since April 2025, HMRC has been de-registering bodies claiming Gift Aid that are not formally registered charities.

-

Is your donor eligible?

Your donor must be a UK taxpayer, sign a Gift Aid Declaration, and pay at least as much in income or capital gains tax as you intend to claim on their behalf in that financial year. From April 2026, higher-rate donors who haven't filed Self-Assessment returns recently may have their Gift Aid tax code relief removed automatically, so encourage them to check.

-

Does the donation qualify?

Donations come in many shapes and forms, and so do HMRC Gift Aid rules. Sadly, not every donation you receive will be eligible. For example, payments for goods and services, Payroll Giving and gifts from companies don’t qualify.

What other HMRC Gift Aid rules are there? Next we'll cover six rules that keep your claims clean and your income flowing. Getting these right means no failed claims, no compliance issues and no money left on the table.

Six HMRC Gift Aid rules to get right

These are the rules that keep your claims clean and your income flowing. Getting these right means no failed claims, no compliance issues and no money left on the table.

1. Individual donors only

Gift Aid can only be claimed on donations from individuals – not companies or collections made on behalf of others. Each donor must make their own declaration.

2. Genuine donations only

The payment must be a voluntary gift, not a mandatory request, membership fee for services, or entrance charge. Simply, it can't be made expecting a benefit in return.

3. No payments for goods or services

If a donor receives anything of material value in return, for example event tickets, merchandise or access to facilities, Gift Aid can't be claimed.

4. Payroll Giving and vouchers are excluded

Donations made via Payroll Giving schemes or vouchers are taken pre-tax, so Gift Aid can’t be applied (it would mean double-claiming relief).

5. No benefit to the donor

Beyond tangible goods, Gift Aid is invalid if your donor receives any benefit in return for their donation. This applies broadly, so if your charity has more complex donor arrangements, it's worth staying alert – especially in light of the 2026 tainted donations update below.

6. Always hold a valid declaration

You must hold a signed, written, or online Gift Aid declaration for every donor you claim on. Without a valid declaration on file, the claim is inadmissible.

GASDS rules: your route to claiming on small donations

The Gift Aid Small Donations Scheme – known as GASDS – is a brilliant companion to the main Gift Aid scheme, designed to tackle one of its biggest practical limitations: the need for a declaration.

Under GASDS rules, you can claim a Gift Aid-style top-up on small cash or contactless donations of up to £30 without needing a declaration from the donor.

If your charity regularly collects cash at events, in a place of worship, or through street collections, this opens up income that would otherwise be impossible to claim.

The key GASDS rules:

- Donations must be cash or contactless payments of £30 or less

- Your charity must already be successfully claiming Gift Aid, GASDS can't be used as a standalone scheme

- Your annual claim limit is currently £2,000 per tax year (£1,250 for prior years)

- Donations must be genuine small, anonymous gifts, you can't split a larger donation to bring it within the threshold

If GASDS isn't already part of your process, it's well worth adding. It's one of those small steps that can add up to a meaningful income stream over time.

What gift aid rules for charities changed in 2026?

The core Gift Aid rules remain the same, but the new tax year bought three specific updates. Here's what you need to know and, in some cases, act on.

Your higher-rate donors may be losing tax relief without realising it

Many higher-rate taxpayers receive additional tax relief on their donations through their PAYE tax code, often without knowing it's there.

From April 2026, HMRC has automatically removed that relief where it has stayed unchanged for three or more years and no Self Assessment return has been filed.

Your charity can still claim Gift Aid on their donations as normal – that doesn't change. But your donors will lose the additional personal relief unless they file a Self Assessment.

A proactive note to your higher-rate supporters explaining the change could be a potential major donor engagement opportunity and a genuine relationship touchpoint.

Membership fee splits now need to be shown upfront

You can only claim Gift Aid on the donation element of a membership fee, not the portion that pays for access to services or facilities.

That rule hasn't changed. What has changed, from March 2026, is timing: you now need to display that split clearly and visibly before someone signs up, not buried in confirmation emails or small print.

If your website, sign-up forms, or renewal communications don't already show the Gift Aid-eligible portion of your membership fee before purchase, it's time to update them. This will both protect your claims, and give members useful information at the right moment.

Tainted donation rules now look at outcomes, not intentions

New Finance Bill legislation means that a donation can be treated as tainted, and Gift Aid reclaimed by HMRC, if a donor receives any financial assistance from your charity connected to their gift, even if there was no deliberate arrangement.

For the vast majority of charities, this simply means being aware it exists. But if your organisation receives large or structured gifts, holds non-standard investments, or has significant legacy income, it's worth taking specific advice.

Your Gift Aid journey starts here

Gift Aid is one of the few places in fundraising where the money is genuinely already yours, and that's the rulebook covered. You know what qualifies, what doesn't, and what's changed.

Get the rules right, stay across the 2026 changes, and you've built a solid foundation for everything that comes next.

Disclaimer: This information is based on the information provided by GOV.UK and HMRC. Always read their guidance for a complete, up-to-date oversight of Gift Aid rules and regulations. Information is correct as of April 2026.